Be honest, have you ever opened your bank app and thought, “Wait… where did all my money go?”

It happens to the best of us. But here’s the truth: when you wing it with your money, you accidentally give your dollars permission to disappear. Winging it almost always leads to overspending, often without you even realizing it.

Budgeting may sound about as exciting as studying for a Chem exam, but it’s one of the most important and practical steps you can take with your money. And the best part? You have the power to make it happen.

A budget is a powerful tool that helps you gain control over your finances. When you have a plan, every dollar has a purpose, and that purpose moves you closer to your goals instead of further away.

Budgeting allows you to clearly see how much money you need to invest, pay your bills, and even set aside for fun. Teens might be able to slide by without budgeting, but if you’re in your 20s, one of the real secrets to long-term financial confidence and success is building the discipline of creating a budget and sticking to it.

A budget doesn’t restrict you. It gives you freedom. Freedom to spend intentionally. Freedom to save strategically. Freedom to feel peace about your financial future.

Proverbs 21:5 says, “The plans of the diligent lead to profit as surely as haste leads to poverty.” In other words, when you make a plan for your money and follow through with discipline, you’re far more likely to see positive results. But if you wing it and hope for the best, you may end up holding your breath the next time you swipe your card at Walmart.

Side note: If you want a masterclass in wisdom, try reading one chapter of Proverbs each day. The financial insight is pure gold!

Let me help you get started with a simple, faith-based money plan that works for your life, not against it (and no, it doesn’t require giving up your iced coffee)!

Watch this video to learn how to stop winging it and start feeling confident with your money:

[How to Stop Winging It With Your Money]

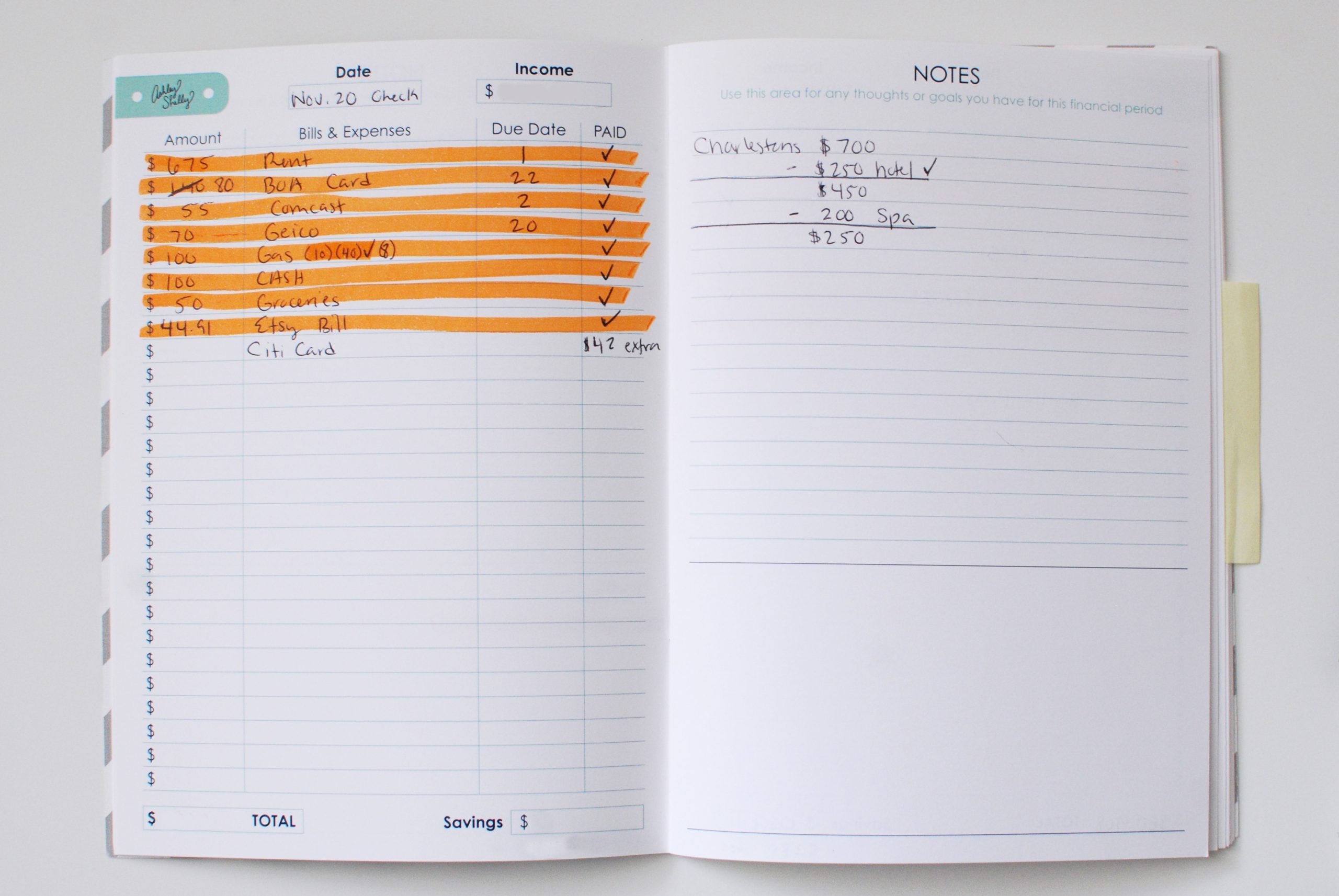

To access the moveHER Money Budget Sheet used in the video, click here.

You can’t control every part of life, but you can choose to plan your money with purpose. And when you do, peace follows.